Banks play an important intermediary role in any economy, transferring money from savers (depositors) to the users of capital (the borrowers). Banks provide the crucial element [capital] to what economists describe as the factors of production which help to drive the country’s economic growth – these include– land, labor, capital, and entrepreneurship.

A well-functioning banking system discharges this intermediation function efficiently while providing other value-added services such as trade facilitation, money transfer, and safety deposit lockers, etc. A sound banking system is also strongly capitalized, and well regulated. If it has these characteristics, the banking system can help provide impetus to economic growth, resulting in the wellbeing of business enterprises and the welfare of the people.

Pakistan’s Banking Sector

Pakistan’s banking sector has a rich history and has undergone several distinct phases. Some banks predate the creation of Pakistan and, by extension, also the central bank. Banks were nationalized in the 1970s, before the 1990s ushered in the first wave of privatizations and entry of new private banks. MCB was among the privatized banks while Bank Al Habib, Bank Alfalah and Askari Bank, among many others, were incorporated in the 1990s.

Competition from Islamic banks have pushed conventional banks to open Islamic banking windows; such as those of Habib Bank and Bank Alfalah.

The second and equally important stage of banking sector reforms commenced in the late 1990s and continued into the early 2000s. This phase saw the restructuring and eventual privatizations of some of the country’s largest banks such as Habib Bank and United Bank.

Transforming them from loss-making and undercapitalized entities to some of the most profitable and valuable banking franchises in Pakistan. This period also coincided with the successful re-launch of Islamic banking (initial launch miserably failed in the 1980s).

Read more: National Bank & Microsoft Deal: Pakistan steps into the next generation…

Meezan Bank was the first Islamic commercial bank to launch in Pakistan in 2002, closely followed by Bank Islami (2005), Dubai Islamic bank (2005), and later existing commercial banks all introduced Islamic windows. Within 15 years, Islamic banking now has around 15% of the overall banking market. Reforms have continued since then, but have been geared towards two broad areas, i.e. improving the stability of the financial system through higher capital requirements, and encouraging greater savings/financial inclusion via a managed increase in deposit rates.

Losses along the way

There have been stumbling blocks along the way the sector saw high provisioning against non-performing loans across 2009-2011, and in 2017-2018, foreign operations of some banks saw large losses. That said, the overall picture remains one of strength, which can be built upon as the banking sector enters the next phase of its lifecycle. This next stage can encompass a greater focus on digital/branchless banking, tighter compliance standards, more robust IT systems, more capital retention, and recalibration in business models to concentrate more on the Pakistani market rather than on foreign operations.

MCB was among the privatized banks while Bank Al Habib, Bank Alfalah and Askari Bank, among many others, were incorporated in the 1990s.

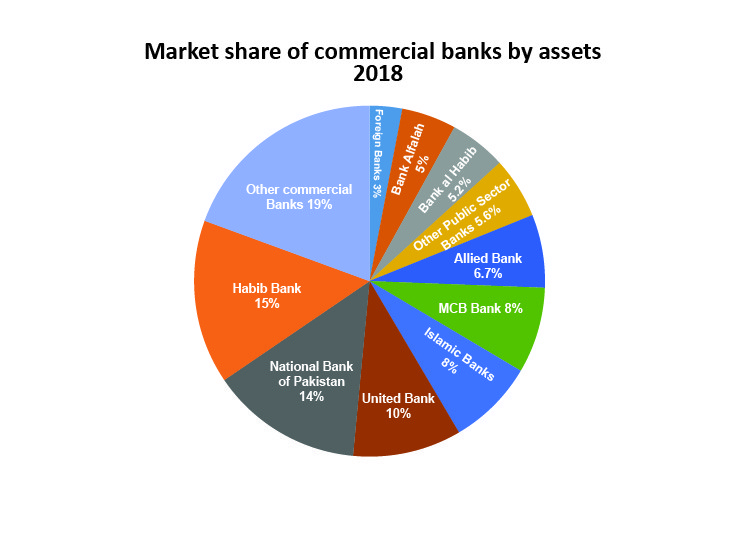

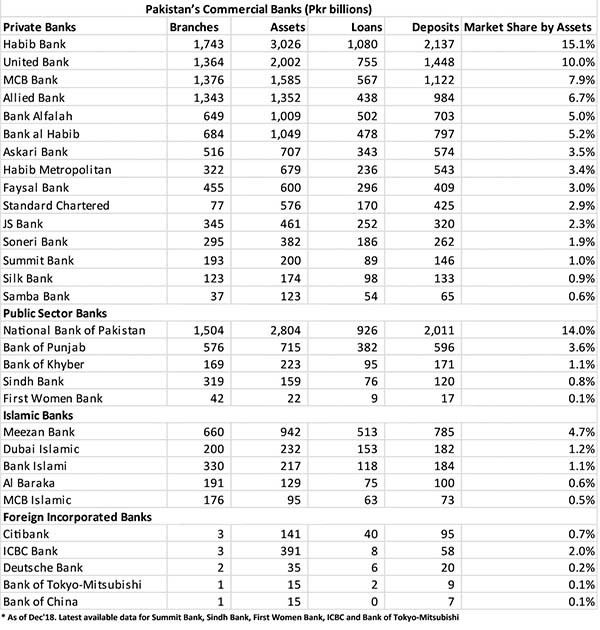

At present, there are 30 commercial banks in Pakistan, a number that has gradually reduced from 36 a decade ago, as a few foreign banks have exited from Pakistan and consolidation has occurred within local banks due to mergers. The sector is dominated by the “Big-5,” i.e., Habib Bank, National Bank, United Bank, MCB Bank, and Allied Bank, which together account for almost 55% of the industry’s assets. However, banks such as Bank Alfalah, and Meezan Bank has grown rapidly over the last few years, challenging the traditional supremacy of the largest banks.

Read more: Pakistan Banking Sector witnesses growth on Digital front and Agriculture

There are relatively few public sector owned banks in Pakistan, they account for around 20% of industry’s assets, unlike India for instance. Islamic banks which started in 2002 have made significant inroads into the market and currently account for around 8% of the market. Meezan Bank is the national champion in Islamic banking and has close to 5% market share of the overall industry’s assets. Competition from Islamic banks has pushed conventional banks to open Islamic banking windows; such as those of Habib Bank and Bank Alfalah.

Need of the Hour

More meaningful competition within the sector, something which the SBP has actively pushed for overtime, is a good thing as it can lead to better rates and services for depositors, and a greater propensity for banks to extend loans even at tighter pricing. Other than the above mentioned Commercial Banks, other categories of deposit-taking institutions in Pakistan include Microfinance Banks (e.g. Khushhali Bank), Specialized Banks (e.g. Zarai Taraqiati Bank), Development Finance Institutions (e.g. House Building Finance Company), Investment Banks and Modarabas.

This article, however, primarily deals with commercial banks. Traditional banking sector models still dominate, but specific trends will become more prominent in going forward. These include the following (not an exhaustive list):

Increased Financial Inclusion

As mentioned earlier, Pakistan is an underpenetrated financial market. Financial inclusion is close to the SBP’s heart and can accelerate through branchless banking and gradual moves to increase documentation in the economy.

Digital Banking

In their 2018 annual reports, a number of large banks have suggested their growing focus on digital banking. This is increasingly expected to be a more competitive space going forward, which can reduce transaction fee as the number of transactions increases. Alipay has recently bought a stake in Telenor Microfinance Bank (Easypaisa), and this can prove to be a fillip in this space going forward. Moreover, other than their in-house development teams, it is likely that banks will look to acquire fin-tech startups going forward.

Read more: National Bank & Microsoft Deal: Pakistan steps into the next generation…

Big Data

Banks have access to millions of customers, and their transaction history and habits can be used to fine-tune and expand service offerings in a more meaningful way.

The Growing Share of Islamic Banking

From less than 10% market share in 2013, Islamic window now comprises around 14% of all banking sector assets in Pakistan. Growth can continue at a fast pace with more banks getting serious in this space, for instance, MCB has recently set up MCB Islamic Bank, a wholly-owned subsidiary.

Better Risk/Compliance Systems

An institution that does not manage risk adequately will not do very well for very long. Given a more robust regulatory backdrop, both at home and abroad, it stands to reason that banks will tighten their risk/compliance functions going forward.

Better IT Systems

This goes hand in hand with some of the trends mentioned above such as big data and digital banking and is already coinciding with higher spending on this front. Moreover, there have reportedly been recent instances of cyber-attacks, and so it is likely that they will focus on improving their IT systems.

Read more: Pakistan Banking Sector witnesses growth on Digital front and Agriculture

More Capital Retention

Capital strength is essential and will continue to remain so. Given that the tax on bonus issues has been removed, it is possible that banks revert to a mix of cash and bonus payouts, as opposed to pure cash payouts over the last few years.

Focus on Domestic Operations

Given that a few large systems have experienced losses in their foreign operations in the last few years, it is possible that international services will be gradually trimmed down in favor of more focus on domestic operations. This is possibly a welcome trend – given Pakistan’s large population size and significant potential for financial penetration, long-term return potential appears to be better in Pakistan than abroad.

New Regulations

Some new regulations that could be introduced across the next few years are the adoption of IFRS 9, and implementation of the Single Treasury Account (TSA). IFRS 9 will compel banks to be more prudent when providing for loans, while the TSA could entail shifting of government deposits to the SBP, which will have to be carefully managed so as not to lead to any systemic risk.

Read more: Pakistan’s Painful Economics, What more the IMF expects?

If capital is essential for economic growth, all efforts have to be made to bring it to the private sector. Capital will enable businesses to grow, in turn allowing them to expand and hire more people. If the environment is conducive, banks will lend. This will require stronger government finances so that the government borrowing to fund its budget deficit does not limit space for private sector credit.

The Balance Sheet

A balance sheet is arguably more important than its income statement. Profitability may vary from year to year depending on various factors, but the underlying balance sheet can help determine the bank’s future trajectory. As with all balance sheets, banks or otherwise, there are two key components – assets and liabilities. Since deposits are an obligation to the depositor, they appear as liabilities on the balance sheet. Similarly, since loans and investments are claims owned by the bank, they appear as assets.

Deposit base of Pakistan, India

Pakistan’s deposit base, generated via 53m conventional deposit accounts, currently stands at above PKR 13.5 trillion (domestic operations only). This appears large but as a percentage of GDP is just 35% vs. 65% in India. In the same vein, only around 20% of Pakistan’s adult population has an account (includes mobile wallet accounts) as opposed to 80% in India; in 2011, it was 35% in India and 10% in Pakistan. This points towards the relative lack of financial inclusion in Pakistan but, over the longer term, can be considered an opportunity.

Pakistan added almost 7000MW of electricity capacity between 2013 and 2018, an increase of 30%, while the Textile sector is the largest export-oriented sector.

The PTI manifesto promised to increase bank accounts to 50% of the adult population. Recently, some of this gap has been met by branchless banking, but this segment remains small – for instance, there are 22.6mn active branchless banking accounts, but on average each account has a balance of less than PKR1,000/=.

However, these accounts are more important for transactional purposes; at least for now. By comparison, the average balance in a traditional bank account is Rs250,000 – which seems high, but the average also includes corporate accounts.

Read more: National Bank & Microsoft Deal: Pakistan steps into the next generation…

Loans given out to Different Sector of Govt.

The outstanding stock of loans in Pakistan is PKR 7.9 trillion, roughly 60% of the deposit base. The balance of deposits is largely diverted towards investments which are dominated by government bonds.

In terms of segment-wise breakup, loans to the Corporate sector (typically large companies) account for around 70% of all loans in Pakistan, with other important categories being loans to finance Commodity Operations (10% of loans), Agriculture (4%), SME (6%) and Consumer (6%).

From a sector perspective, the two largest borrowers are Energy (15% of loans) and Textile (14% of loans). This is not surprising – Pakistan added almost 7000MW of electricity capacity between 2013 and 2018, an increase of 30%, while the Textile sector is the largest export-oriented sector. It is worth mentioning that loans to public sector entities are now 16% of loans, up from 5% in 2007.

Reasons behind Lack of Credit Penetration

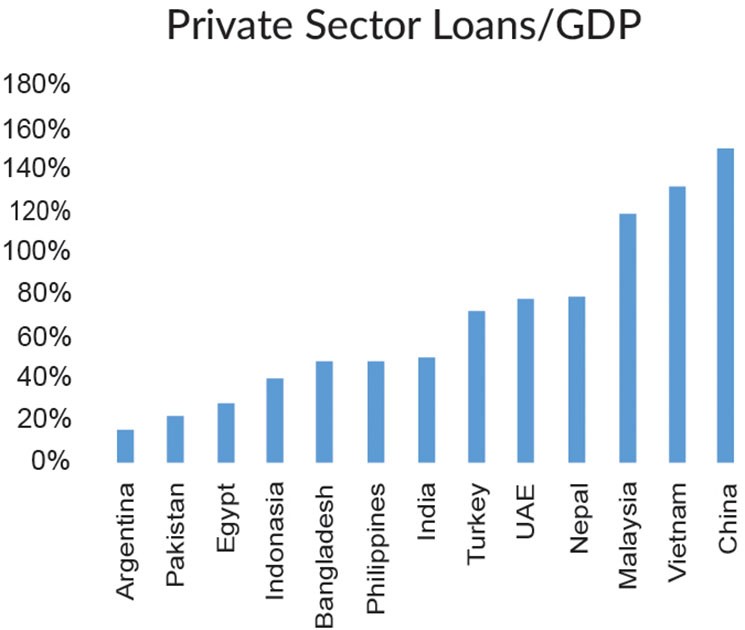

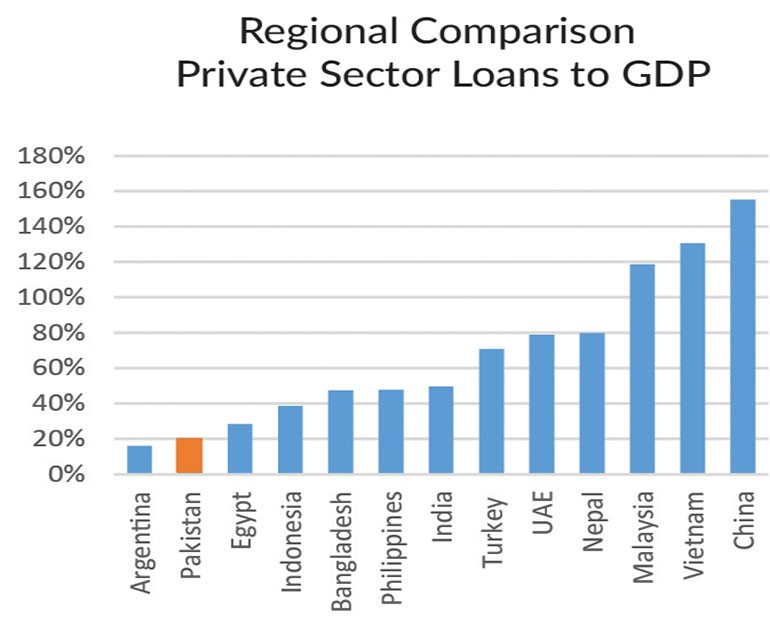

Loans equate to around 20% of GDP in Pakistan, which is low given this proportion stood at more than 25% of GDP back in 2007. Low credit penetration is a function of several factors including, but not limited to:

High Crowding Out

Both the government itself, as well as public sector enterprises, are large borrowers from the banking system, which reduces space for private sector credit. A smaller fiscal deficit, which will need greater tax revenues, can help reduce this crowding out.

Cautious Lending Stance in the Last Decade

Banks were exuberant lenders in the early to mid-2000s, propelled by a post-privatization surge. However, a high percentage of loans turned bad in the global financial crisis (2008/09) after which banks have been cautious.

This is most visible when tracking the higher-risk SME, and Consumer segments – loans to SMEs have reduced from 15% of loans in 2007 to 6% of loans now, while loans to Consumer have also reduced from 13% to 6% of loans. Pakistan has been through several boom and bust cycles, and staying cautious is a logical choice for such institutions, at least until macroeconomic stability becomes more long-lasting.

Structural Deficiencies

Weak foreclosure laws and high property prices (partly due to the gap between officially notified DC rates and market prices) are key reasons behind the negligible mortgage loan market in Pakistan, in contrast to global economies where private housing is an essential engine of economic growth.

Read more: Pakistan Banking Sector witnesses growth on Digital front and Agriculture

The Income Statement

The interplay of assets and liabilities reflects on the income statement. Key heads on the income statement are net interest income (and provisions), non-interest income, expenses and, of course, profits.

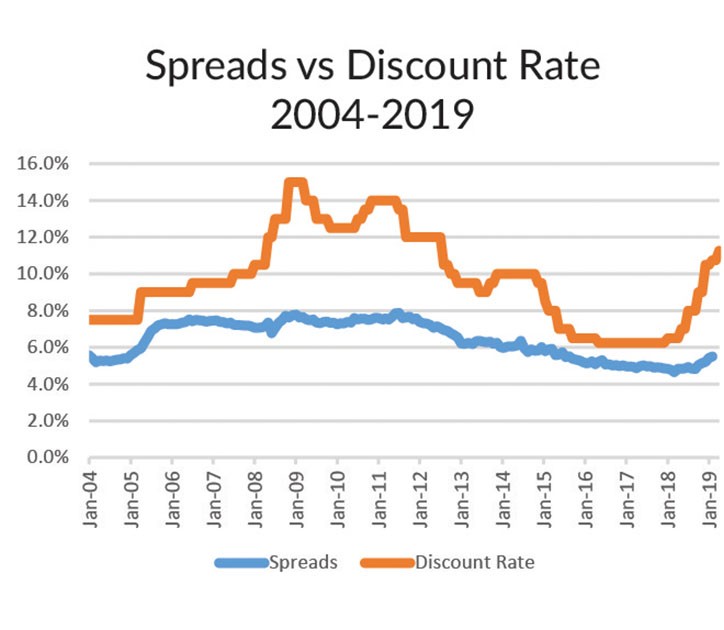

Net Interest Income

This is the difference between interest income and interest expense. Interest is earned on assets such as loans and investments, while interest expense is incurred on liabilities such as deposits. The margin on interest earned on loans and interest expensed on deposits is known as the spread i.e. the differential that banks charge for their intermediation services (the difference between interest rates earned on all interest-bearing assets and the rate charged on all interest-bearing liabilities is known as Net Interest Margins i.e. NIMs).

Pakistan remains a high spread market – 5.50% in Feb’19, but the spread has significantly reduced over time given it was as high as 7.9% in mid-2011. Some reasons behind this reduction are

- lower exposure to the higher risk but also higher-yielding SME and Consumer segments,

- more competition in lending to the Corporate sector which has led to tighter pricing,

- greater lending to public sector enterprises which, due to risk free nature, may pay a lower interest rate compared to private sector entities, and

- a rate floor set by the SBP on savings deposits (the most popular class of deposits in Pakistan). The floor is currently 8.75% which is set by a formula: discount rate – 2.5%. This rate floor does not exist for Islamic banks or products.

Read more: Pakistan’s Painful Economics, What more the IMF expects?

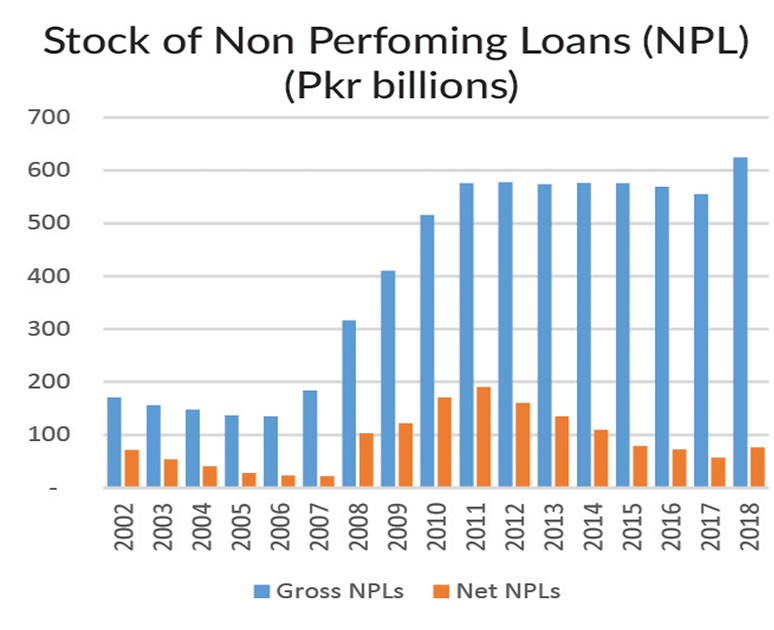

Asset Quality

Given that loans are not always repaid, the spread that banks earn is not risk-free. If a loan goes bad, it must be written off as a loss or provided for. Given that interest rates have risen rapidly in the last 15 months, and the economy is experiencing a slowdown, it stands to reason that asset quality will deteriorate in the near term.

Pakistan’s deposit base, generated via 53m conventional deposit accounts, currently stands at above PKR 13.5 trillion . This appears large but as a percentage of GDP is just 35% vs. 65% in India.

This has already commenced – after remaining stable over the last several years, the stock of Non-Performing Loans (NPLs) for commercial banks has increased from PKR554bn at end-2017 to PKR624bn at end-2018 (Pakistani banks typically do not write off NPLs, so this stock represents legacy NPLs as well). It is likely that further NPL formation will take place going forward.

That said, asset quality deterioration should not be as bad as in the 2008-11 cycle. This is due to:

- Lower exposure to the higher risk SME and Consumer segments, compared to 10 years ago

- More exposure in government securities and public sector entities

- More cautious lending over the last several years

- High level of bad loans that have already been provided for (high coverage)

- A less leveraged corporate sector compared to the past

Read more: NBP avoids banking sector woes, achieves highest revenue

Non-Interest Income

Other than net interest income, the second key earnings component on the income statement is non-interest income, which can include fee income, dividends, foreign exchange income, and capital gains, among others.

Of these, the most critical line item is fee income. Some easily understandable fee income contributors are commissions on ATM transactions, L/C charges, cheque book fee, commission on remittances, etc. These small fee sum up to a large amount – in 2017, total fee income earned by the banking sector was in excess of PKR 100 billion!

Admin Costs

No intermediation can take place unless banks generate deposits. As a result, expenses incurred on deposit gathering activities constitute the bulk of admin expenses for banks, although IT-related expenses are also becoming an important part of expenses. Intermediation expenses are largely to do with branch-related expenses such as rents, utilities, and staff salaries.

Given that admin costs are typically around 50% of a bank’s total income, the opportunity available to purely branchless banks is visible. There are banks abroad that operate solely on the branchless model and save significantly on costs. In Pakistan however, the traditional brick & mortar business model still holds sway.

Read more: Branchless banking arrives to AJK to help those without bank accounts

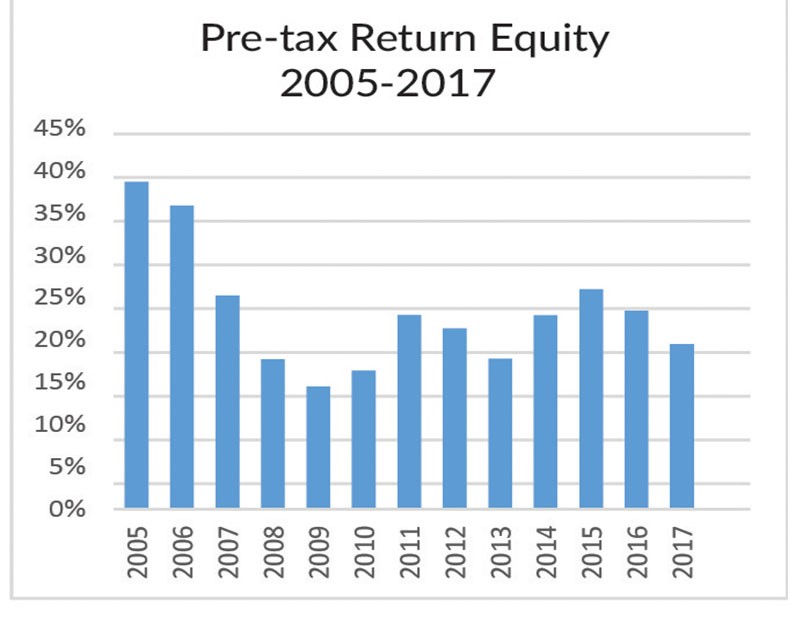

Profitability & Returns

Profitability depends on factors such as balance sheet size and structure, deposit mix, loan mix, margins (spreads), asset quality, non-interest income, and cost efficiency. A sound banking model will have diverse income streams. Two other essential factors are taxation and capital strength. In Pakistan, banks face a 35% corporate income tax rate as well as the 4% super tax (introduced to resettle IDPs).

The base 35% rate is already higher than the 29% rate for non-banks and confirms that governments typically tend to tax the banking sector at higher rates (Pakistani inst. have in the past been taxed at more than 50%). Similarly, a balance sheet growth is limited by the size of its capital. Over the last decade or so, the SBP has pushed for higher capital strength. These factors must be kept in mind when assessing banking sector profitability.

The sector’s ROE has reduced from a peak of 26%+ in 2005 to low double digits at present. This is partly due to higher effective taxation (32% in 2005 to 41% in 2017) and stronger capital (the sector’s CAR has increased from 11.3% in 2005 to more than 15% at present). Over the next few years, it is expected that the banking sector ROEs will reach late teens.

Raza Jafri serves on the Board of the CFA Society Pakistan and brings over 10 years of experience in sell-side equity research. He is currently associated with Intermarket Securities Limited. Earlier, he was the Head of Research at AKD Securities Limited. He was awarded “Best Analyst of the Year 2015/16” by CFA Society Pakistan and was also recognized for “Best Banks Coverage” by AsiaMoney in 2012.

The views expressed in this article are the author’s own and do not necessarily reflect the editorial policy of Global Village Space.