Given the emerging economic and political environment, it is pertinent to highlight the risks emerging on the political front and their implications for the economy and capital markets. The government’s hesitation in making difficult decisions, such as delaying the removal of energy subsidies, created pressure on capital markets.

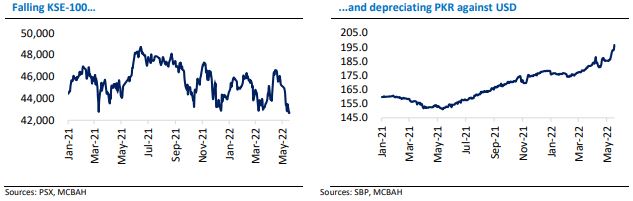

In May 2022 alone, the government’s indecision has caused the KSE-100 Index, the benchmark for stock exchange performance, to lose 2,523 points (5.6 percent), and PKR lost around 5.6 percent against USD to reach 196 against a Dollar and went to an all-time low of 202.56 on May 26, 2022. Treasury Bills (T-Bills) yields on average increased by 30 basis points, touching levels not seen since 1998. T-Bills reflect where markets see inflation going and thus interest rates.

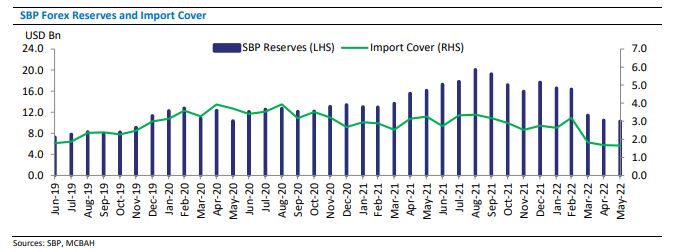

FX reserves stand critically low

The importance of remaining in the IMF program has become critical for the country, as its reserves now stand at a 23-month low of USD 10.3 billion, barely enough to cover two months of imports. This has put the government in a fix; their decision to increase pump prices, which has eroded their political capital, was a necessary one to remove Pakistan from the brink of a sovereign default.

Severity requires immediate action

With such a low level of reserves, the government will have to make a decision fast, either fulfill the IMF requirements to avoid default or go for early elections so the caretaker government can make all the difficult decisions that will protect the political capital of the PDM government.

Clarity on IMF program may calm the markets

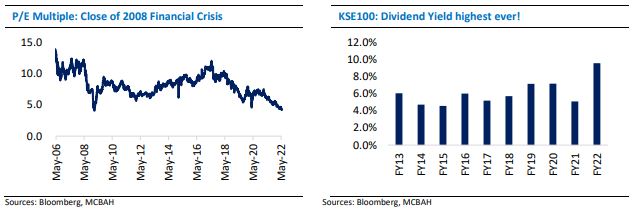

Either way (caretaker or current government taking harsh decisions) will be positive for the market as it may pave the way for much-needed IMF program and macroeconomic adjustments. The market is currently trading at a Price to Exchange Ratio (PER) of 4.8x, which is close to levels seen in the financial crisis of 2008. In fact, the current PER is even lower than the March 2020 levels when Covid-19 ravaged the equity markets across the globe. Furthermore, the dividend yield of KSE currently stands at the highest in recent history, depicting the deep discount the market is trading at.

Read more: Pakistan Economic Survey 2021-22 unveiled

Rising subsidies are swelling the deficit

Petroleum prices in the international market continue to map a rising trajectory since March 2022, when the government announced to keep pump prices constant. The government had earmarked PKR 104 billion to keep pump prices constant for almost four months (pump prices have been increased by Rs. 60 by the time of writing). However, due to rising international prices, the government was spending PKR 120 billion per month. Similarly, PKR 65 billion are now required per month to keep the power tariff unchanged compared to PKR 150 billion earmarked for four months (electricity prices were increased by Rs. 7.91 per unit by June).

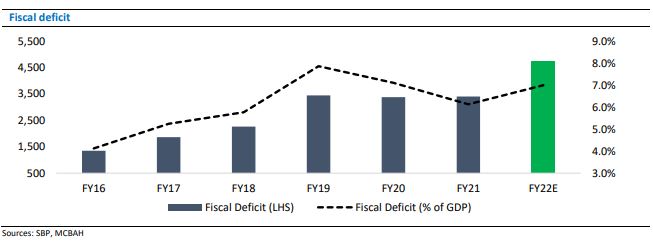

The sheer size of these subsidies was unsustainable and put a considerable strain on the fiscal deficit, which analysts expect to swell to PKR 4.7 trillion (7 percent of GDP), compared to last year’s number of PKR 3.40 trillion (6.1 percent of GDP).

Subsidies are encouraging consumption

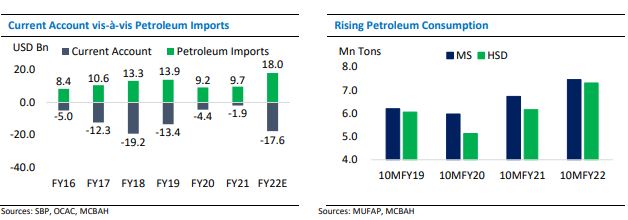

Energy subsidies are not only squeezing fiscal space but also keeping our energy import bill high. Lower energy prices encourage consumption, evident from the highest ever oil import bill of USD 2.2 billion in April 2022. Similarly, diesel and petrol sales jumped 14 percent and 17 percent YoY to 0.8mn tons and 0.9 tons, respectively.

This was the highest ever diesel consumption in a month. Removal of subsidies is critical to reining demand pressures to cool off the widening current account deficit, which has already jumped to USD 13.2 billion during nine months of this fiscal year. The ongoing commodity supercycle (in the aftermath of post-Covid demand recovery and Russo-Ukrainian conflict) is expected to keep energy and food prices higher, which is expected to widen CAD to USD 17.6bn (4.6 percent of GDP) for FY22, the highest since FY18 when the country suffered a CAD of USD 19.2 billion (6.1 percent of GDP).

Read more: Pakistan’s economic growth to pick up pace in FY23?

Inflation expectations are rising

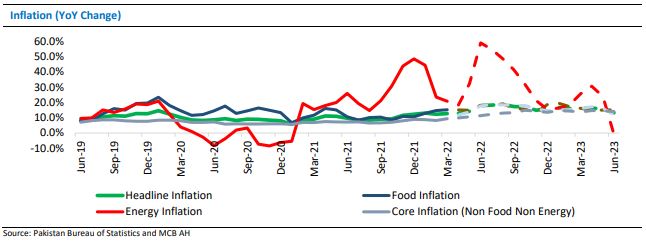

CPI-based inflation for April 2022 jumped to 27 month high of 13.37 percent, taking a 10MFY22 figure of 11 percent compared to 8.6 percent in the same period last year. The commodity supercycle is the major contributor to rising price levels in the economy. With already a high inflation base, raising the energy tariff may push the inflation up to an average of around 12 percent for FY22, and a sustained price level may inch up the inflation to the north of 15 percent in FY23.

Interest rates could jack up further

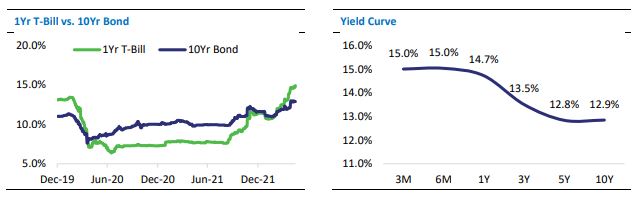

Yields in the fixed income market have already started incorporating the widening fiscal deficit and higher inflation expectations going forward. One-year T-Bill is already trading around 2.45 percent above the SBP policy at 14.7 percent, the highest since 1998. SBP is expected to raise interest rates by 1-1.5 percent in upcoming monetary policy in response to rising inflation expectations and discourage aggregate demand.

However, the inverted yield curve is also incorporating the scenario of normalization in interest rates going forward, with five years and ten years bonds trading around 12.9 percent, much lower than shorter tenures.

This Information was taken from Investor Letter “Economic imbalances and its implications” produced by MCB-Arif Habib on May 18th, 2022, and updated numbers where needed by GVS.