The mortgage industry in any country supports more than 40 Allied industries such as steel, cement, chemical, glass & ceramics, transport banking. All of these industries combined contribute more than 30% in GDP.

When these industries grow, not only do they increase the GDP but consequently increase capacity in the employment force, which is another stimulus for a growing economy.

In high-income economies, mortgages are widely available and routinely used for consumer financing of housing. Many low and lower-middle-income countries only register a few thousand loans or a few hundred in some cases.

As an example, the mortgage to GDP ratio in Bangladesh stands at above 5 percent, while in India stands at more than 11 percent.

In Pakistan, this ratio stands at a mere 0.3 percent, which is significantly lower than the South Asian average of 3.4 percent. Pakistan, as a result, faces a deficit of more than 10 million housing units, which increases by nearly 0.4 million units per year.

Read More: Role of Banks in Mortgage Financing

The supply of housing, especially for low-income groups in the country, remains negligible despite high demand. As per a recent IFC study on Pakistan’s housing market, only 1% of housing supply caters to 68% of the population earning a monthly income of up to US$ 188, while approximately 56% of housing units cater to 12% of the population earning a monthly income of more than US$ 625 and most Financial Institutions are only limited to Tier 1 cities for their mortgage finance products.

Other factors contributing to the low Mortgage to GDP ratio are high property prices due to urbanization, rising construction costs, unavailability of fixed-rate mortgage financing, ineffective foreclosure laws, and issues with land titles that make the Financial Institutions lend selectively.

In order to overcome these challenges, the Government of Pakistan, particularly in the last few years, took various steps; one of them was to set up a mortgage refinance company to address the funding constraint which was hindering the growth of the primary mortgage market.

Pakistan Mortgage Refinance Company (PMRC) was therefore set up as a Mortgage Liquidity Facility by the State Bank of Pakistan to address the long-term funding constraint in the banking sector.

PMRC was formed in 2015 and commenced its operation in 2018, over the years, PMRC has acted as a catalyst in the housing financing sector, whereby it is providing long-term financing to primary mortgage lenders at subsidized and fixed rates, enabling them to launch mortgage products for end consumers particularly in the low- and middle-income segment.

Read More: General Anwar Ali Hyder Chairman (NAPHDA): Unpacking The Low-Cost Housing Initiative

PMRC provides both refinancing and pre-financing products, which enables the primary mortgage lenders to offer affordable and accessible mortgage financing solutions for their customers. Primary Mortgage Lenders (PMLs) generally finance their assets with short-term

deposits and prefer keeping their liabilities short-term, leading to mortgage finance loans for 10-12 years only.

While making long-term financing available, PMRC helps PML’s to reduce their asset-liability mismatch. The market is seeing mortgage loans with tenor up to 20 years. Such longer tenor loans reduce monthly installments improving the affordability of mortgage loans for end-borrowers.

In its offerings, PMRC has various financing products under both conventional and Islamic modes of finance. It has already partnered with eighteen financial institutions, including several commercial banks, MFB (Micro Finance Banks), MFI (Micro Finance Institutions), DFI (Development Financial Institutions), and Non-Banking Finance Company (NBFC), which are engaged in housing finance.

Read More: JS Bank and PMRC sign an agreement to promote affordable housing finance

PMRC has ensured that its funding outreach is not only concentrated in a single area but spans across Pakistan, covering all provinces from Northern Areas of Gilgit Baltistan to Baluchistan and the deserts of Sindh.

Increasing diversity in ownership through women’s participation is promoted through pricing incentives made available for PMLs. Over these years mortgage portfolio funded by PMRC has created 26 percent women participation in home ownership.

It has also promoted funding for increasing home ownership in rural districts and communities through partner institutions like Thardeep Microfinance which have introduced a new culture of house financing in such areas.

These efforts have given recognition to PMRC with a “AAA” entity rating and being nominated for most innovative and best contributing Non-Bank entity in Pakistan Banking Awards. PMRC is now regarded as the fastest growing DFIs in the country.

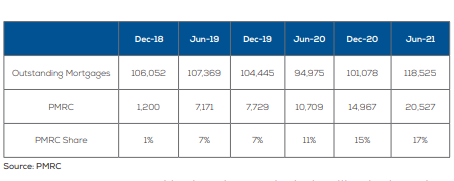

With the mortgage market growing from PKR 107 billion in June’2019 to PKR 118 billion in June‘2021, PMRC mortgage refinancing grew by PKR 13 billion, reaching 17 percent of total mortgage financing in the country in just three years of its operation.

Besides providing housing finance facilities, PMRC has developed a credit guarantee product specifically for low-cost housing. This product is offered through a unique trust established by the Government of Pakistan, where PMRC acts as a Trustee and is directly funded by the World Bank group. The trust provides credit guarantee of up to 40% on first-loss basis to primary mortgage lenders.

The guarantee allows them to partially alleviate their credit risk emanating from low-income housing portfolios and thus encouraging them to lend in this segment. As of now, PMRC has executed credit guarantee agreements with 13 primary mortgage lenders.

PMRC has also been engaged in assisting PMLs with standardization of financing documents, product development, and providing trainings. The company is recognized as a knowledge Partner at forums of the International Mortgage Market Association (ISMMA) and Asian Secondary Mortgage Market Association (ASMMA). PMRC has also provided advisory for product development to Mortgage Refinance Companies of Kenya, Saudi Arabia, Tajikistan, and Uzbekistan.

Read More: Pakistan’s Failure to promote Low-Cost Housing? A Historic Overview

PMRC is also an active capital market issuer and has issued various debt securities, both conventional (Term Finance Certificates) and Islamic (Sukuks). Since FY20, PMRC has issued a total of 7 fixed income instruments worth PKR 12 billion. It introduced a first of its kind Sukuk with a unique structure based on a pool of mortgage receivables. It remains the only DFI in Pakistan that is issuing fixed-rate medium and long-term debt instruments to support capital market development.

Pakistan was one of the first countries to adopt Sustainable Development Goals (SDGs) goal 11 on creating resilient communities. PMRC is working to ensure access to adequate, safe, and affordable housing. It aims to continue providing the needed impetus for growth of the mortgage market bringing new asset classes supporting green housing for higher social and environmental standards and encouraging the market to innovate with better and efficient digitally enabled and low-cost housing solutions.

PMRC remains committed to increasing accessibility and affordability for financial inclusion and greater home ownership in Pakistan.